Our prior article discussed how to determine if a company falls under the CSRD requirements and its approach to reporting (What does the CSRD mean for UK companies?). The next step is to understand the scope of reporting requirements which are determined by topic applicability to an organisation and thus the work needed to comply with the CSRD.

European Sustainability Reporting Standards (ESRS) and Topics

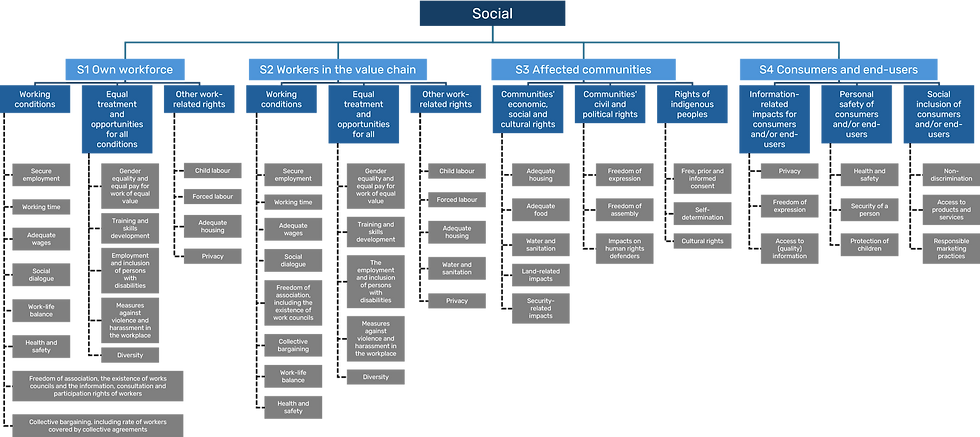

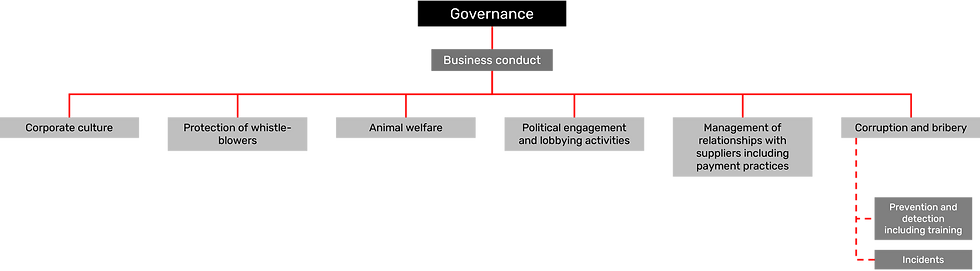

The Corporate Sustainability Reporting Directive (CSRD) in total outlines up to 1,052 possible datapoints for companies to report against. But reporting to all datapoints is not mandatory. The datapoints prescribed by the CSRD fall across 12 European Sustainability Reporting Standards (ESRS). The ESRS cover General Disclosures (ESRS 2) as well as standards for Environmental (ESRS E1, E2, E3, E4 and E5), Social (ESRS S1, S2, S3 and S4) and Governance (ESRS G1) topics, whilst ESRS 1 outlines General Requirements, i.e. approach and methodologies, rather than specific datapoints.

Each ESRS topic is actually subdivided into sub-topics and sub sub-topics, which allows for more granularity to be applied from the double materiality assessment and topic mapping process which will be discussed later on in this article.

The following diagrams provide a breakdown of all Environment, Social and Governance topics, sub-topics and sub sub-topics as defined within the CSRD. This is not an exhaustive list of possible topics to report against but gives an indication of the broad nature of the topics. Under the requirements of the CSRD, any material impact, risk or opportunity within these topics should be reported against.

The large number of topics and sub-topics may seem daunting at first glance, but not all will be applicable to your business and what you report is determined by the a Double Materiality Assessment.

First Steps – Structure & Gap Analysis

The following steps outline the processes used to determine the scope of your CSRD reporting requirements:

Double Materiality Assessment: identifying sustainability related impacts, risks and opportunities which are material to your organisation.

ESRS Topic Mapping: linking the identified topics to the corresponding ESRS topics.

Assurance Confirmation: agreement on your double materiality assessment process and the resulting alignment to ESRS topic standards.

ESRS Data Gap Analysis: a gap analysis to compare existing disclosures to the datapoint requirements.

Double Materiality Assessment

Within the double materiality assessment (DMA) companies should apply a dual-lens approach that covers both impact and financial materiality.

Impact materiality relates to the organisation’s impacts on people or the environment related to sustainability matters (inside-out approach) including employees, communities, and the environment (both direct and indirect, actual and potential). Impact materiality considers aspects beyond financial metrics, such as climate change, human rights, diversity, and supply chain practices.

Financial materiality relates to the financial impacts of sustainability matters on the organisation’s performance, financial viability and long term value creation (outside-in approach). This involves identifying risks and opportunities that could have a financial impact on the business.

The results of a DMA will be used to inform the topic mapping process but will also serve to inform your organisation’s overall strategy. Expected results from a DMA exercise should include:

Identification of impacts, risks and opportunities (IROs) that could have significant implications for the organisation and its stakeholders

Risk prioritisation to identify high-risk areas that require immediate attention

Opportunity identification to recognise options that may benefit the organisation

Materiality Matrix whereby sustainability issues are mapped based on their significance to the organisation (financial materiality) and its stakeholders (impact materiality)

ESRS Topic Mapping

The purpose of the ESRS topic mapping step is to determine the scope of ESRS topics your organisation will have to report against, considering those that are deemed material your organisation. In some instances your organisation’s material topics will be entity specific, therefore not directly aligned exactly to the ESRS topics, which will require some

interpretation.

Assurance Confirmation

Following the DMA and ESRS topic mapping steps, we recommend that an organisation obtains feedback from its assurance provider over their process and results. Whilst not mandated by the CSRD, it forms a useful precautionary measure to confirm that the work done to scope an organisation’s CSRD reporting is appropriate before investing further time and resources on the potentially numerous future workstreams.

ESRS Data Gap Analysis

Having defined the ESRS topics to report against an organisation will then need to identify:

What disclosure requirements are mandated under the topics regardless of materiality?

How is the data expected to be disclosed? Is it narrative, semi-narrative, numerical, etc.?

When is the organisation expected to disclose this information? The phased in nature of some disclosure requirements may only expect certain disclosure in an organisation’s 4th year of CSRD reporting for example.

Is the disclosure mandatory or voluntary?

Our service

At CEN, we are able to help guide your organisation in reporting against the CSRD by helping conduct a Double Materiality Assessment to determine what topics and sub-topics are material to your organisation as well as helping organisations answer the above questions.

Our proprietary CSRD tool determines which datapoints are applicable to your business, where there are gaps in your data and when you are required to report the phased-in disclosures.

Our tool covers all 1,052 data points across all ESRS topics, the suite of aspects (risks assessments, policies, metrics, targets, actions) and data types (narrative, semi-narrative, numerical, dates) prescribed by the CSRD.

Further steps

The steps outlined in this article form just the beginning of an organisation’s CSRD journey, but they play an important role in forming the scope and basis of future workstreams.

No companies report to the degree required by the CSRD and following the determination of what to report, companies potentially face a large list of actions, data, processes and disclosure that they need to develop in order to comply with the CSRD.

Though it may vary depending on the scale of an organisation, the following steps provides an outline of the potential scale of this undertaking.

Contact Us

CEN helps business maximise their sustainability potential, performance, and ESG disclosure.

For more information about our services pertaining to CSRD, Double Materiality Assessments and Regulatory Compliance, please get in contact and our team would be happy to assist.

Jasper Crone: Director

Roger Johnston: Director

Comments